In this article, I will delve into the world of Microeconomics from the perspective of a Producer/Manufacturer.

Producer Theory, in simple terms, defines the interactions between the market forces and how producers interpret it and use it to maximize their profit. It is somewhat similar to Consumer Theory (link), with mild, subtle differences that when panned out over an extended timeframe, can lead to varied conclusions.

So let’s dive into it.

Production Function

A firm’s decision to produce so many goods is always affected by many factors. Notably, some worth considering are the workers employed, their wages, the cost of production, the amount of capital invested, and the list goes on.

For simplicity’s sake, we will assume that the production level of a firm notably depends on two major factors —

Labor — No. of workers employed.

Capital — Money invested in machines and equipment.

So, using them let’s define our production function.

where,

q = amount of quantity produced (demanded).

k = Capital

L = Labor

Now, for better analysis and understanding, we will assume a production function such that it works for most of the cases.

|

|---|

| Our ‘assumed’ production function. |

Even though it looks pretty similar to the Utility function we assumed in our previous discussions on Consumer Theory, it can behave very differently when considering different timeframes.

Assumption — q is always equal to the quantity demanded in the market. No less or no more.

Short Run Production

Imagine this, you’re a company boss!….You are to propel the production level of your firm. How are you going to do it? Well, using our production function, one might say — ‘We can increase either L or k, or both simultaneously’. Fair enough? Well, let’s complicate it.

Think about it, let’s say you only want to increase your production in the short term i.e. You don’t want to commit huge resources to get a permanent increase in production, but rather interested in a temporary fix. Examples for this case, would be a start-up founder, who is willing to go public or expecting a hefty investment from a VC in the upcoming months. So rather than burning his own pockets in buying heavy machinery and factories, he will simply consider having few more workers to ooze out that extra return until the money comes in.

Also, it looks much better on your balance sheet when your debts are low, irrespective of how much profit you make.

I hope that helped.

Now coming to the main topic, what happens in the short term? Well, as you might have guessed it, you’re Capital invested remains constant.

Nobody buys a home only to live there for six months.

So, your production function (q) becomes —

where,

k bar — some constant.

L — Labour employed.

q — Production level (quantity produced).

Now, my q is dependent only on L i.e., to increase my production level in the short term, I only need to increase the Labour employed.

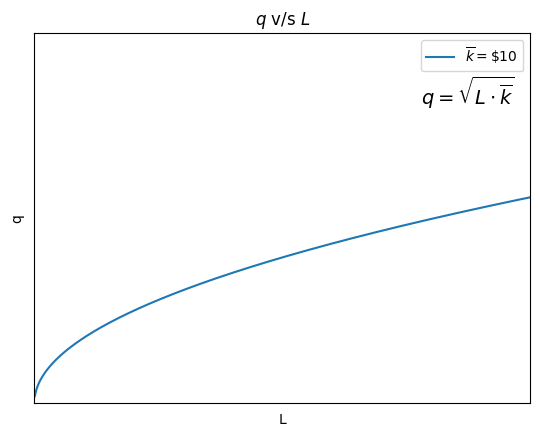

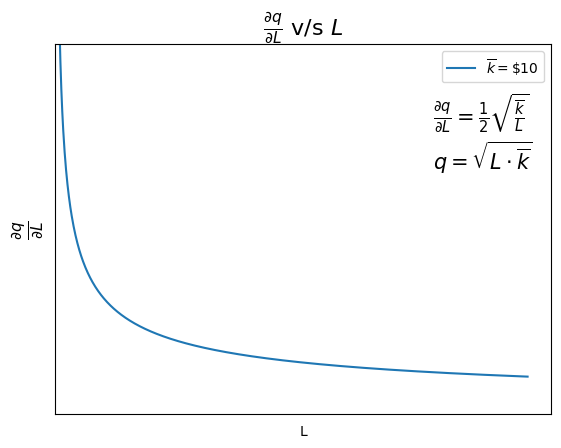

Let’s plot q v/s L.

k is constant i.e. $10

Can you make out something peculiar from the graph?

Firstly, we see that q increases with L i.e., when we increase the Labour employed, the production level automatically increases. Mathematically —

The slope is equal to 0 when L->infinity.

But then, there’s one more exciting thing to note — The slope of the graph decreases as L increases. Mathematically, it signifies —

Practically, what does this mean? Well, you might have guessed it — When L increases, the additional L does less good. In other words, the extra labor does less good for the production level of the firm.

This is also known as Diminishing Marginal Product of Labour.

|

|---|

| The Marginal Product of Labour is decreasing in nature. |

Why does this happen? Well, if you remember, we assumed k to be constant for this case. Hence, an increase in labor won’t do much good when the number of machines and equipment needed to produce the goods remains constant.

At first, when L is small, it does not matter, but when L is large, all machines are already in use, and an extra L won’t do much good.

Makes sense, right?

Now, we’ll move on to Long Run Production. We’ll again visit this idea of short-term production when discussing Costs.

Long Run Production

Now that you know what short-term production means? Surely you remember we assumed some factors to be constant and made our analysis based on that. Yep, it was k, the Capital Invested (machinery, equipment, factories).

Now, assuming k to be variable, we get our production function as —

where,

q = Production Level

k = Capital invested

L = Labour employed

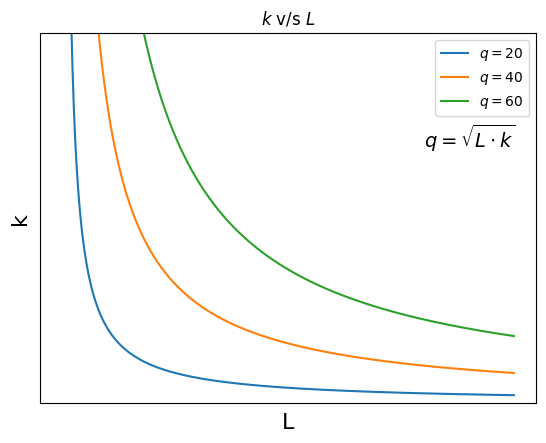

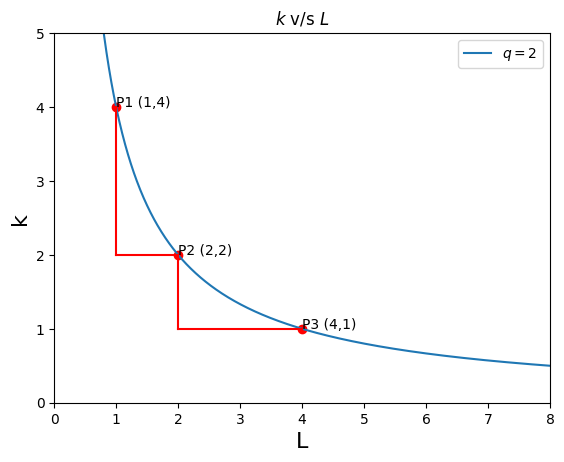

Let’s plot the graph of L and k for some values of q —

These hyperbolic lines are known as Isoquants, or if you are familiar with Indifference Curves from Consumer Economics, you can say that they are the ICs for firms. Practically, what they mean is that for every combination of L and k in the curve, it is going to give the same corresponding output i.e. q (production level).

‘Isoquant’ in Latin means ‘equal quantity.’

To understand this concept better, let’s plot some different production functions and analyze them —

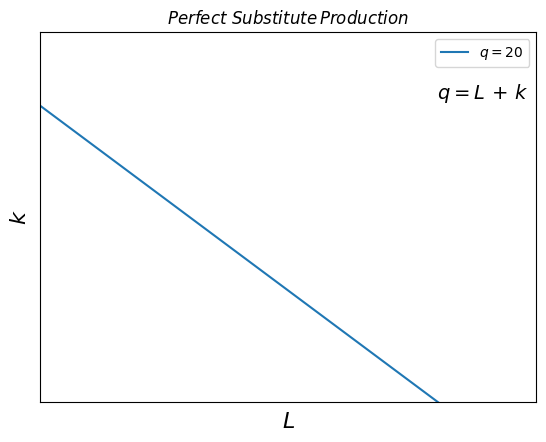

This is the Perfect Substitute Production Function —

It means that here, L and k can be interchanged, and the output still remains the same.

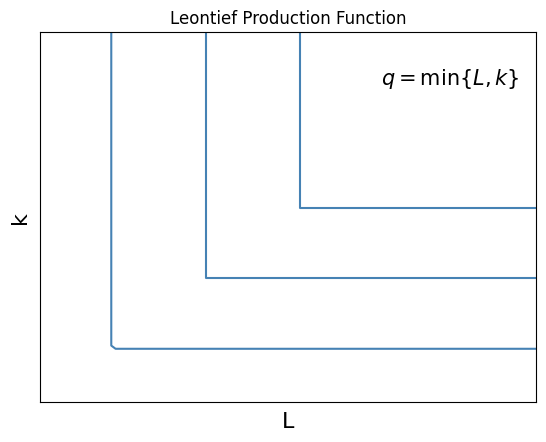

Then, we have the Leontief Production function —

This is an exciting function that simply says that the production level is only equal to the minimum of L and k. Let’s take an example:

In the production of automobiles, let L be the number of steering wheels and k be the number of gearboxes. A car will only be complete when both items are present. Hence, no. of cars produced (q) will be —

Makes sense, right :)?

For further reading, you can also check out the Cobb-Douglas production function (link).

Fine? Let’s move on…

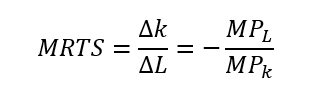

Marginal Rate of Technical Substitution

This might sound scary and long, but is nothing but the slope of the Isoquant :)

Plotting the Isoquant again with the slope calculation —

From P1 to P2, the modulus of the slope is high (=2) i.e., intuitively, it means that from P1 to P2, we gave up 2 units of capital and instead gained 1 unit of Labour. Hence, Labour has relatively more value here.

Similarly, from P2 to P3, we see that we gave up 1 unit of Capital to gain 2 units of Labour. Here, the cards are reversed, Capital has relatively more value than Labour. What’s going on? Well, If you are aware of how Indifference Curves work in Consumer Economics, then you might’ve guessed it, the reason from P1 to P2, the values of k were quite large compared to L, hence you would be willing to give up a lot of k to gain an unit of L. Think about it, a factory where you have all the machinery and equipment but no labourers to work. You’ll be willing to give a lot of that machinery just to gain an additional laborer. At the end of the day, you need at least the minimum number of laborers to produce goods!

Same case with P2 and P3 as well. You have an excess of Laborers but a shortage of equipment to produce the goods.

Mathematically, we define MRTS as:

What do you think the MRTS for the Leontief production function will be? :)

Before we jump into Costs, there are a few more minor topics I would like to discuss, and their relevant links will also be mentioned in case of further reading.

Returns to Scale

Returns to Scale simply mean how much the production level increases/decreases when the inputs are scaled. Not clear? just look at the cases:

Constant Returns to Scale —

In this case, when the inputs are doubled, the output (q) is also doubled.

Examples —

Bread Production: Doubling the amount of wheat almost leads to a proportional increase in bread production.

Increasing Returns to Scale —

In this case, when the inputs are doubled, the output level turns out to be more than double.

Examples for this case would be:

Internet-Based businesses: Putting your website on the web just costs a little (inputs), but the output can turn out to be huge as the number of customers accessible is potentially infinite.

Pharmaceutical industries: A significant increase in R&D cost can lead to the developing a new drug that can potentially serve millions of additional customers.

Decreasing Returns to Scale —

Similarly, in this case, doubling the inputs do not reflect in the doubling of the output.

Examples —

Artisan or Handcrafted products — These products always have a less yet constant demand in the market. In fact, their demand and customer sentiment are derived from the lack of easy availability of such products in the market. Similar is the case with luxury brands.

Bespoke products — Imagine this: if today Rolls Royce decided to double their staff and machinery in hopes of producing more Rolls Royces’, do you think the customer sentiment is going to remain the same? No right? Because similar to the previous example, it derives a significant chunk of its value from its absence from mainstream automobiles. Their demand is going to drop.

Production and Innovation

Population, when unchecked, increases in a geometrical ratio, and subsistence for man in an arithmetical ratio.

- Thomas Malthus in the Essay on Principle of Population (1798).

I believe you have heard this sometime during your lifetime. This simple statement screams at us the need for population control if we are to sustain for the long term.

The scientist who wrote this, Thomas Malthus, was an interesting figure. To remind you, it was in 1798, when victories of the French and American Revolution and the superior ideas of Liberalism and Democracy were still ringing in people’s minds. Everyone expected mankind to be on the path to perfection. After all, when you have a government who actually cares about the population, what could possibly go wrong? But there’s Thomas Malthus, who believed that the way humanity is moving forward is destined for doom rather than perfection. Why? Because of the population growth. He calculated such elated enthusiasm is bound to increase the population ‘geometrically’ and with a friendly government around, who’s there to stop them? With such increase in population, the factory as well as agricultural output has to increase as well, but as we know there are only so many acres of arable land that can be cultivated. After that limit is reached, misery is bound for humanity.

Thomas Malthus — ‘The Dismal Scientist’

You can read his essay — On the Principle of Population here.

Is he wrong? Indeed, his logic seems robust. But here we are, 2 centuries later, and the world never seemed better.

So where was he wrong??? Guess..

Well, he was correct about the limited amount of arable land, after all the size of the Earth is still the same even after centuries of human development. But the arablity of the land is something he did not consider. In general terms, it is the ‘Innovation factor’. Even though we have the same (or more) amount of land as 2 centuries ago, but the production output levels today far outnumber what was then. This is thanks to new innovations such as machine tractors, genetically modified crops, fertilizers.

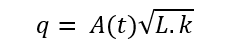

Hence, returning to our original discussion, to account for the productivity factor in our initial production function q. We add a productivity part as well, which changes(increases) with time.

where,

A(t) = Productivity function

L = Labor employed

k = Capital employed

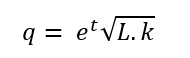

For e.g. let’s take the q as -

Here, we assumed the production function to be e^t. Therefore, at t=0 and t=t1, to produce the same output q0, less no. of L and k will be required for t=t1, as e^t1 will give a high positive value and, hence, subdue the effect from the other variables.

This resonates with our intuition that when time passes, innovation kicks in, and now more of the work can be done using less resources. Intuitive right?

Conclusion

I believe this discussion should end here only considering how lengthy and intensive it turned out to be. Next blog, I’ll be discussing what affects the production costs (labor wages, rents) and how do producers decide to produce the quantity that maximizes their profits while keeping the costs at a minimum.

Do drop your comments if you have any doubts and I’ll try to answer them to the best of my ability. Thank you.